RETIREMENT

AND THE CENTS BEHIND IT

Retirement is NOT

Retirement. One word may conjure a myriad of images or emotions including how much money you need to have in the bank or invested in the stock market to retire. However, making the decision to retire is less about how much you have saved and MUCH MORE about how much you SPEND. According to the consumer credit reporting agency, Experian, the average total debt per American consumer in 2024 topped $105,000. This figure includes an average of $6,730 for credit cards, $19,014 for personal loans, $45,157 for HELOC loans, $35,208 for student loans and $252,505 for mortgages. While mortgage and housing expenses are required parts of life, revolving lines of credit (ex. person loans and credit cards) are more about the choice of how you want to live.

Once upon a time in our lives, we had much of the same revolving debt as every other American. Then, we analyzed our own spending habits and slowly began to reduce the debt. As we killed one type of debt after another, we were able to use our “extra” money to pay off other debts faster. We celebrated as milestones were met. Looking at retirement was very easy when we confidently exclaimed that we were DEBT FREE!

About Money in the Bank

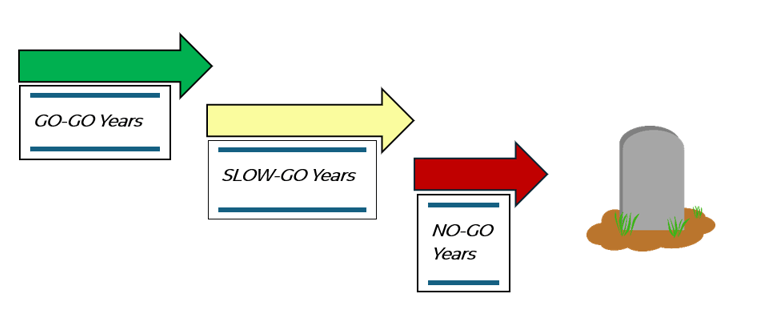

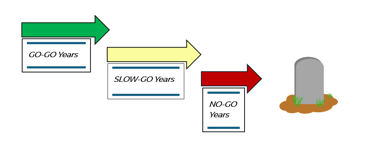

The Phases of Retirement

There are generally three phases of retirement for you to consider. The length of each phase will vary by person. Genetics and life history play a large role in the life expectancy of people.

First is the GO-GO phase. At this stage of retirement, you are likely happy, healthy, and excited to enjoy life to the fullest. You may want to join activities you put off while working or travel.

Second is the SLOW-GO phase. During this stage, you might start settling down, letting go of some of the hobbies or activities you have been doing. There may be health factors that start impeding some of your actions and abilities.

Third is the NO-GO phase. This phase will look very different depending upon the person. In this phase, the body shuts down more. It might even need nursing care.

Since the length of these phases is unknown, the length of retirement is unknown. In 1935 when the Social Security Act was enacted, the life expectancy (at birth) was 58 years old for men and 62 years old for women. IN the United States today, the average life expectancy of men is 77.22 years and women is 82.11 years. These statistics, as well as your family and health history, may help you decide when to retire.

We Retired Early

From youth through retirement, there are logical practices we should consider as we move from working life to non-working life. While not financial advice, we share ideas to consider if you want to achieve early retirement or any retirement.

Should You?

Following The Stones

followingthestones@gmail.com

Authentic people posting original content, photos and lived experiences.