Did We Win the Lottery?

To afford long-term travel, we must be rich, right? WRONG! Read our real-life example.

FEATURED ON HOMEPAGERETIREMENT

7/9/20265 min read

NO, we didn’t win the financial lottery. But we did win the dating lottery. Online dating in your 40s and 50s is beyond terrible until you find a real partner; someone with common interests, common work ethics, common beliefs, & common compassion. Greg and I were lucky to find each other in that world of online dating and with one simple question, our paths were sealed. NO, it wasn’t a marriage proposal, it was a proposal to retire and travel. But how can we afford to retire and travel? Greg was 61 and I was a mere 52.

It started with moderate frugality in our personalities. We had each been natural savers. When our kids were grown and we started the empty nest life, we were able to pay off the last of our debts and compound our individual savings even more. Together, we held tight to the ideas of being debt-free. After 4 years of dating (2020-2024), when we decided to move in together, we also had to decide what to do with two houses, two jobs, and common dreams.

Houses, Jobs, and Stuff

We each owned a house in separate towns and neither of us liked the idea of quitting our current job to find a new one in the other town. After meeting with two financial advisors, a CPA, and using online software, we were assured that the financial blocks were solid between us. We BOTH decided to leave our jobs and retire early. We each began selling things we didn’t need, duplicate items were common and easy to purge quickly. Then, I sold my 2- bedroom, 1-bath house while the market was good. I sold my car which had been paid off for years. Since his house had a maintenance free yard, I didn’t need my lawn mower, weed-eater, chainsaw, or hand tools. I was mimicking the people on YouTube who sold everything to travel the world. Except, I did it to move in with Greg.

EXPENSES

Retired or not, we must be honest about expenses. People who don’t track their expenses never have the confidence to retire and travel. Successful travelers know their general living expenses and budget for their preferred lifestyle. Very few travelers live like the rich and famous, but all can define their preferred lifestyle. For example, some people sell everything and choose to live nomadically; other people use geoarbitrage to live with less expenses; still others choose to maintain a home base in the USA and slow-travel in longer durations to keep costs affordable. Knowing the balance of financial resources compared to expenses is key. As stated above, we were able to cut our expenses dramatically, as a couple, just by moving in together, but not everyone can win that lottery. We realized that stopping our extraneous expenses that “made us feel good” was the best way to fund our retirement plans whether we were going to travel or not.

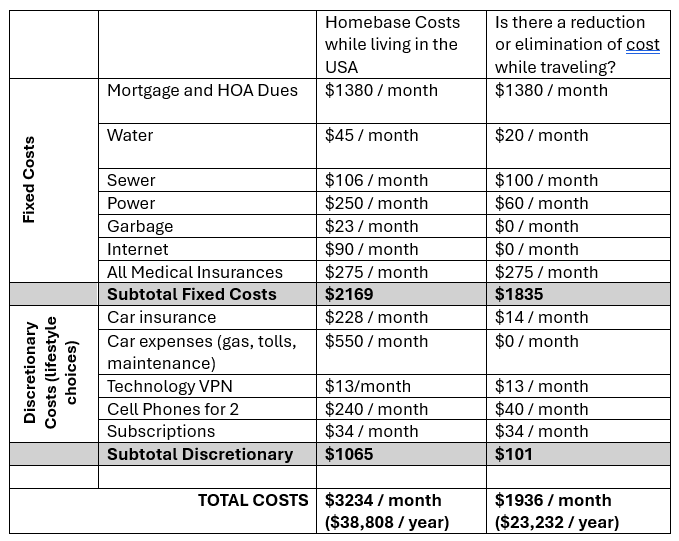

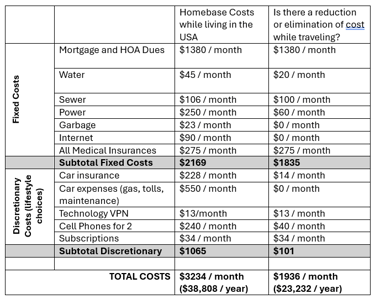

Nowadays, our only debt is the mortgage we carry, because maintaining a homebase was more convenient to us than selling everything. Beyond that mortgage, 100% of everything else is paid off and our success was being able to compound our income instead of compounding the debt. In our retirement, we looked at our financial numbers from every angle possible. We consulted professionals and professional tools to assist us in making our decisions, but you will need to make your own decisions. Below is the snapshot of OUR expenses for OUR home base in Washington State, everyone will have different numbers. Look at how costs change when we shift to travel mode.

Health Care

One of the most significant concerns in retirement is health care. Thankfully, we don’t have chronic medical issues with intensive treatment plans. Greg has physical limitations due to his service in the infantry, but as a Marine his health care in the USA is covered by the V.A.. He will be able to add Medicare on top of that V.A. coverage when he turns 65-years-old, but it will still only be health care in the USA. I am not so lucky. For the moment, I am pleased to have benefits through the affordable care act (A.C.A.) for as long as it lasts. This care covers me in the USA with minimal out of pocket expenses and thankfully, I don’t need significant medical care.

When we’re traveling abroad, we pay for private medical insurance without USA coverage. The plans we choose cover catastrophic care, if needed, while we are in another country or onboard a cruise ship, but not routine care and not care in the USA. When coverage in the United States is removed from the insurance equation, health care costs around the world are much more budget friendly. Here are our real examples.

April 2025-April 2026 (12 months) - 2 Adults covered by WorldTrips – Total Cost $2,778.00

April 2026 to October 2026 (6 months) - 2 Adults covered by WorldTrips – Total Cost $1419.00

Again, these insurance plans are in place for catastrophic medical needs, and we will pay cash for pharmaceuticals, lower level or routine medical care if we need it while traveling.

None of our insurance plans cover dental or vision. These must be budgeted like any other monthly expense. Since we both wear progressive glasses, we found a wonderful USA insurance plan for vision services through VSP that covers BOTH of us for only $34.00 per month ($408.00/year). After comparing many dental plans and analyzing our dental needs, we found it to be cheaper paying out-of-pocket for this care than to purchase an insurance plan. Whether we get dental care at home in the USA or abroad for a fraction of the cost, we added annual care into our annual budget. So, we can choose routine medical care at home in the USA provided by VA or ACA, or we can pay out-of-pocket for medical, dental, or vision services abroad. Read more on these subjects in these BLOG posts.

Income Buckets

Given our lengthy work history with multiple employers, we have a combination of employer-based savings accounts, personal savings accounts, and government "savings" accounts. Using the bucket strategy, we each have income streams for our future selves. Neither of us have ever taken a loan from our income streams, nor have we cashed them out when separating from one employer to work for another employer. Now, our buckets will support a long-term retirement plan for us, but we must abide by the federal rules of withdrawal to avoid being taxed to death on the future income streams. Under each category are the ages at which we can legally withdraw from them.

Conclusion

As you can see, we did not win the state financial lottery. OUR income buckets were earned across almost 90-combined years of time in the workforce and OUR expenses are as small as we could make them while living in the USA or abroad. Today, we are enamored with each other and the life we have chosen together in this retirement lottery game. Your successful retirement requires knowing your income buckets, planning your fixed and discretionary expenses, staying as healthy as possible, and having fun.

As you can see from our example, the cost of living in the USA is still there, but thankfully, those home-base costs reduce by 40% while we are traveling. Will we sell our home base? Likely, but we still haven’t decided what that would look like for us. For now, every country we visit has different cost of living expenses for housing, groceries, transportation and entertainment. We can select the country based on how expensive or cheap we want to live over the year. We will continue to track our expenses while traveling abroad and those numbers will continue to be balanced alongside our home expenses for our total annual budget. Again, some people choose to eliminate the USA home, but everyone has different needs and numbers. KNOW your numbers NOW. Scratch your own lottery ticket and win your best retirement.